ITR Filing Guide for Govt Employees in Delhi NCR

Best ITR Filing Guide for Government Employees in Delhi NCR (FY 2025-26 | AY 2026-27)

Let's be honest — most government employees in Delhi NCR think ITR filing is simple because their employer deducts TDS every month. "My office handles it," is what you hear in the corridors of Central Secretariat, South Block, or the DDA offices. But here's the thing: TDS is just your employer's estimate. The actual return — with the right form, the right deductions, and the right regime — is entirely your responsibility.

And when you get it right, the difference can be thousands to lakhs of rupees back in your pocket.

This guide is built specifically for you—the central government officer, the state government teacher, the PSU executive, the CRPF constable, the railway employee—who works and lives in Delhi, Noida, Gurgaon, or Faridabad. Let's walk through everything step by step.

Who Is This Guide For?

This guide applies to:

- Central and State Government employees (IAS, IPS, IRS, Group A/B/C)

- Public Sector Undertaking (PSU) employees (NTPC, BHEL, ONGC, etc.)

- Defence and Paramilitary personnel stationed in Delhi NCR

- Railway, Postal, and other departmental staff

- Delhi Government / Municipal Corporation employees

- Pensioners receiving a government pension

Step 1 — Know Your Income Head as a Government Employee

Government employees earn income under "Salaries" as defined in Section 17 of the Income-tax Act. This includes:

Basic Pay — Fully taxable, forms the base for all other calculations.

Dearness Allowance (DA)—Fully taxable for central government employees. As of January 2025, the DA rate is 53% of basic pay for central government employees.

House Rent Allowance (HRA) — This is where Delhi NCR residents get a significant advantage. Since Delhi is classified as a metro city, you can claim HRA exemption of up to 50% of your Basic+DA under Section 10(13A), provided you are paying rent and filing under the old tax regime. This exemption is not available under the new tax regime.

Leave Travel Concession (LTC/LTA) — Exempt from tax for travel within India, claimable twice in a block of four calendar years. Current block: 2022–2025. The exemption covers only the cost of travel (air, rail, or bus) and not hotel stays, food, or sightseeing expenses.

Children's Education Allowance — Up to ₹100 per month per child (for a maximum of 2 children) is exempt, a modest but claimable benefit.

Transport Allowance for Specially-Abled Persons — ₹3,200 per month is exempt under the new tax regime as well.

Perquisites — Official vehicles, rent-free accommodation (common for IAS/IPS officers), and employer-paid telephone bills are either exempt or valued at concessional rates for tax purposes.

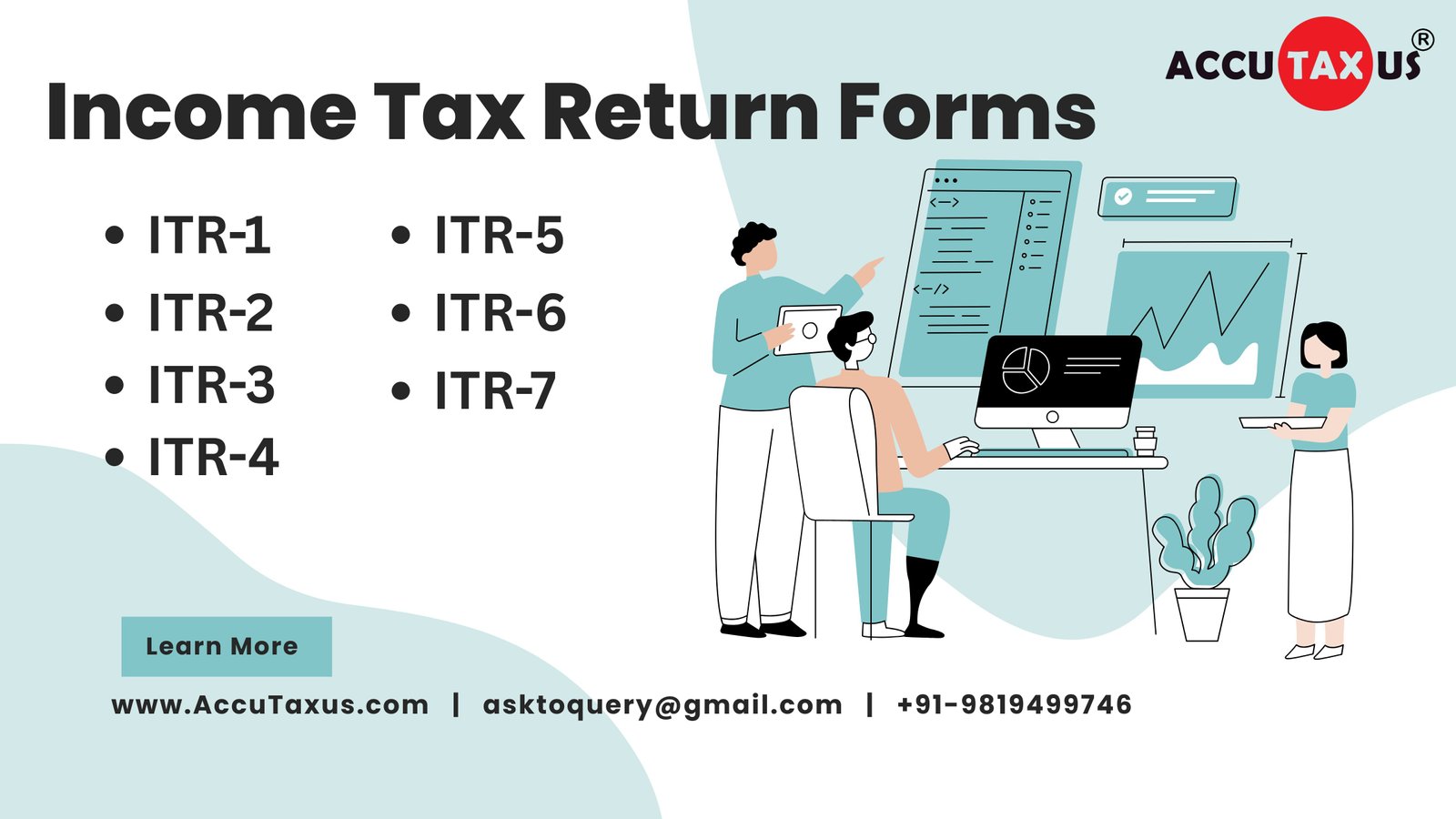

Step 2 — Choose the Right ITR Form

This is where many government employees go wrong.

ITR-1 (Sahaj) is the right form if:

- Total income from all sources is up to ₹50 lakh

- Income is from salary/pension + up to two house properties + interest + LTCG under Sec 112A up to ₹1.25 lakh

- You are a resident Indian (not RNOR or NRI)

- You do not hold foreign assets or are not a director in any company

ITR-2 is required if:

- You have income from more than two house properties

- You have capital gains beyond what ITR-1 allows (e.g., from shares, property sale)

- You are an RNOR or NRI

- You are a director in a company (even a private limited one)

- You hold foreign assets

The vast majority of government employees will file ITR-1. However, if you sold a flat, invested in mutual funds with significant gains, or have property income from multiple sources, move to ITR-2.

Step 3 — Old Tax Regime vs New Tax Regime — Which Is Better for You?

This is the most important decision you make before filing. Since AY 2024-25, the new tax regime is the default. If you want to file under the old regime, you must explicitly opt out of the new regime each year (in the ITR itself, for salaried individuals with no business income).

New Tax Regime — Slabs for FY 2025-26 (AY 2026-27)

| Income Slab | Tax Rate |

|---|---|

| Up to ₹4 lakh | Nil |

| ₹4 lakh – ₹8 lakh | 5% |

| ₹8 lakh – ₹12 lakh | 10% |

| ₹12 lakh – ₹16 lakh | 15% |

| ₹16 lakh – ₹20 lakh | 20% |

| ₹20 lakh – ₹24 lakh | 25% |

| Above ₹24 lakh | 30% |

Key: Under the new regime with the rebate under Section 87A, taxable income up to ₹12 lakh attracts zero tax for resident individuals. Add the ₹75,000 standard deduction and a government employee earning a gross salary of ₹12.75 lakh pays zero tax.

Old Tax Regime — Slabs for FY 2025-26

| Income Slab | Tax Rate |

|---|---|

| Up to ₹2.5 lakh | Nil |

| ₹2.5 lakh – ₹5 lakh | 5% |

| ₹5 lakh – ₹10 lakh | 20% |

| Above ₹10 lakh | 30% |

In the old regime, you can claim HRA, LTA, 80C investments (PPF, ELSS, LIC — up to ₹1.5 lakh), 80D health insurance (up to ₹25,000), 80CCD(1B) NPS own contribution (up to ₹50,000), and several other deductions. These significantly bring down your taxable income.

Which Should You Choose?

New regime tends to work better if:

- You have fewer deductions to claim (e.g., you live in a government quarter and don't pay rent)

- Your gross salary is below ₹12.75 lakh (you'll pay zero tax)

- You don't have a large home loan

The old regime tends to work better if:

- You pay high rent in Delhi NCR, and the HRA exemption is significant

- You have a home loan with large interest payments

- You invest heavily in 80C instruments (PPF, NPS, insurance)

- Your total deductions exceed ₹3–4 lakh

Our strong advice: calculate both before you file. The Income Tax Department's portal has a built-in calculator, and Accutaxus Consultancy can run a comparison for your specific situation.

Step 4 — Key Deductions Government Employees Should Not Miss

Under Both Regimes

Standard Deduction — ₹75,000 (new regime) or ₹50,000 (old regime). No documents needed; it's automatic.

NPS Employer Contribution — Section 80CCD(2) — This is the most powerful deduction available under the new regime for government employees. Your employer's contribution to the National Pension System Tier-I account is deductible up to 14% of Basic + DA for government employees (10% for private sector). This is available in both regimes. If your basic pay is ₹50,000/month, 14% = ₹7,000/month = ₹84,000 per year — all tax-free even under the new regime.

Under the Old Regime Only

Section 80C — Up to ₹1.5 lakh from investments in PPF, NSC, ELSS mutual funds, LIC premiums, GPF contribution, children's tuition fees, home loan principal repayment, and Sukanya Samriddhi.

Section 80CCD(1B) — Own contribution to NPS Tier-I, up to ₹50,000 additional deduction over and above the 80C limit.

Section 80D — Health insurance premiums up to ₹25,000 for self/spouse/children; additional ₹25,000 for parents (₹50,000 if parents are senior citizens).

Section 80E — Interest on education loan for higher studies (self, spouse, or children), with no upper cap, deductible for 8 consecutive years.

Section 10(13A) — HRA Exemption — For Delhi-NCR residents paying rent, the exempt HRA is the least of the actual HRA received, 50% of Basic+DA, or the rent paid minus 10% of Basic+DA.

Section 10(5) — LTC — Claimable twice in a block of four years for domestic travel with family.

Section 80G — Donations to PM Relief Fund, Charitable institutions, etc.

Step 5 — Documents to Keep Ready Before Filing

Do not sit down at the Income Tax portal without these:

- Form 16 (Part A & Part B) from your employer/DDO — this is your primary salary TDS certificate

- Form 26AS — downloadable from the IT portal; reconcile all TDS entries

- Annual Information Statement (AIS) and Tax Information Summary (TIS) — newer, comprehensive statements that include bank interest, mutual fund transactions, and property registrations

- PAN and Aadhaar (both should be linked; mandatory)

- Bank account details (pre-validated on e-filing portal for refund credit)

- Rent receipts and landlord's PAN (if annual rent exceeds ₹1 lakh, PAN of landlord is mandatory for HRA claim)

- Investment proofs — LIC, PPF passbook, NSC certificates, ELSS statements

- Home loan interest certificate (if applicable)

- Health insurance premium receipts

- NPS statement from CRA (NSDL/Protean)

Step 6 — Deadlines and Penalties You Must Know

The deadline for most government employees (ITR-1/ITR-2) for FY 2025-26 is July 31, 2026.

If you miss this deadline:

- Late filing fee under Section 234F: ₹1,000 if income is below ₹5 lakh; up to ₹5,000 if income exceeds ₹5 lakh.

- Interest at 1% per month on unpaid tax under Section 234A.

- Loss of carry-forward: Capital losses and business losses cannot be carried forward if the return is filed late.

- Loss of regime choice: Late filers cannot opt for the old tax regime — the new regime becomes mandatory.

- Delayed refunds: The sooner you file, the sooner your refund (if any) is credited.

Belated return can be filed up to December 31, 2026, under Section 139(4), with penalties.

Revised return can be filed up to March 31, 2027, under Section 139(5) — if you made an error in an original return, this is how you fix it.

Special Situations for Delhi NCR Government Employees

You live in a government quarter (General Pool Accommodation): The value of the accommodation is treated as a perquisite and is already added to your taxable salary by your employer. You cannot claim HRA. This is a common misconception — government employees in quarters often assume they have no accommodation-related tax liability when in fact it's been included in your Form 16 already.

You have taken voluntary retirement (VRS): VRS compensation up to ₹5 lakh is exempt under Section 10(10C). Gratuity received on retirement is exempt up to ₹20 lakh under Section 10(10).

You are receiving pension: Government pension is taxable as salary. Pensioners can claim standard deduction of ₹75,000 (new regime) or ₹50,000 (old regime). Family pensioners receive a deduction of the lower of one-third of the pension or ₹25,000 per annum under the new regime.

You have transferred cities within NCR: If you moved from Ghaziabad posting to Delhi mid-year, you may have received transfer allowance / packing allowance. These are partially exempt — only actual travel and packing expenses are non-taxable; the balance is added to income. Your Form 16 should reflect this correctly. If it doesn't, you must self-declare it.

You have income from property (house in hometown): If you rent out property in your home city while living on HRA in Delhi, both can be claimed under the old regime — HRA exemption AND home loan interest deduction — provided the two cities are different.

Common Mistakes Government Employees Make While Filing ITR

1. Not reconciling AIS with Form 26AS. The AIS has far more information — including bank FD interest, mutual fund redemptions, and dividend income. Failing to report these can trigger notices.

2. Claiming HRA under the new regime. HRA is not available under the new tax regime. Claiming it anyway will lead to a defective return notice.

3. Forgetting to declare interest on savings accounts. Even if it's ₹5,000 in savings bank interest, it must be reported under "Income from Other Sources." (However, up to ₹10,000 of savings bank interest is deductible under Section 80TTA in the old regime.)

4. Using the wrong ITR form. If you sold a flat in Gurgaon, you cannot file ITR-1. You must use ITR-2.

5. Not e-verifying the return. Many employees submit their returns but don't complete e-verification. Without verification within 30 days, the return is treated as not filed.

6. Ignoring Form 10E before claiming arrear relief. If you received salary arrears (e.g., from a pay commission revision), you need to file Form 10E on the portal before filing your ITR to claim relief under Section 89(1).

7. Not checking the TDS mismatch. If your DDO made an error in depositing TDS against your PAN, it won't appear in 26AS. You need to follow up with your accounts section to fix this before filing.

Why Work with Accutaxus Consultancy?

Government employees across Delhi NCR — from the IAS officer in Lutyen's Delhi to the clerk in the North Delhi Municipal Corporation — trust Accutaxus Consultancy for one reason: accuracy.

Unlike generic online portals that auto-fill and auto-submit, Accutaxus brings a qualified expert to your specific situation. We:

- Review your Form 16 and AIS line-by-line

- Run a detailed old regime vs new regime comparison for your income

- Identify every deduction you are entitled to claim (and many miss)

- Handle NPS, HRA, LTC, and arrear calculations correctly

- File on time so you never pay an avoidable penalty

- Represent you before the Income Tax Department if a notice is received

We serve government employees across Delhi, Noida, Greater Noida, Gurgaon, Faridabad, and Ghaziabad.

📲 Visit www.accutaxus.com to get started or book a consultation today.

Quick Reference Checklist for Government Employees

- Collect Form 16 (Part A + Part B) from your DDO

- Download Form 26AS and AIS from the IT portal

- Reconcile salary, TDS, and interest income

- Decide: old regime or new regime? Run the comparison.

- Gather rent receipts (HRA claim under the old regime)

- Collect investment proofs for 80C, 80D, NPS

- Check if Form 10E is needed (salary arrears, pay commission)

- File on or before July 31, 2026

- E-Verify within 30 days of filing

FAQ

Q1. I live in a government quarter in Delhi — can I still claim HRA? No. If you live in government-provided accommodation (like Central Government Pool Accommodation), HRA exemption cannot be claimed. Your perquisite value is already computed in your Form 16.

Q2. Is the new tax regime better for me as a central government employee? It depends on your deductions. If you pay high rent, have a large home loan, or invest heavily in 80C instruments, the old regime may save more. If you live in a government quarter and have fewer deductions, the new regime often results in lower tax due to the higher exemption limit and zero-tax threshold at ₹12 lakh.

Q3. Can I claim both HRA and home loan interest at the same time? Yes — but only under the old tax regime, and only if the property for which you have the loan is in a different city from where you are posted. This is common for Delhi NCR government employees with property in their home cities.

Q4. What if my employer deducted excess TDS? Will I get a refund? Yes. If TDS deducted exceeds your actual tax liability (calculated after all deductions), the excess is refunded by the Income Tax Department directly to your pre-validated bank account after your return is processed.

Q5. I received DA arrears this year. How do I handle it in my ITR? You can claim relief under Section 89(1) which ensures you are not taxed at a higher rate because of arrear income. You must first file Form 10E on the income tax portal before filing your ITR. Failing to do so will result in the return being flagged.

Q6. What is the last date to file ITR for FY 2025-26? For most government employees filing ITR-1 or ITR-2, the deadline is July 31, 2026. Missing this date attracts a penalty of up to ₹5,000 and interest at 1% per month on unpaid tax.

Q7. I am a retired government employee receiving a pension. Do I need to file ITR? Yes, if your total income (pension + any other income) exceeds ₹3 lakh (old regime basic exemption for senior citizens aged 60–80 years) or ₹5 lakh (super senior citizens above 80). Pensioners should also file to claim refunds of TDS, if any was deducted.

Q8. My Form 16 shows less income than my AIS. What should I do? AIS captures data from banks, mutual funds, and registrars. If there's a mismatch, first check why (FD interest not declared to employer, dividend income, etc.) and include all income in your ITR. Filing based on Form 16 alone while ignoring AIS can lead to income tax notices.

Trending Posts

-

Annual Survey of Incorporated Services Sector Enterprises (ASISSE)

2026-07-02 04:06:05

Annual Survey of Incorporated Services Sector Enterprises (ASISSE)

2026-07-02 04:06:05

-

ITR Filing Guide for Govt Employees in Delhi NCR

2026-06-23 12:19:45

-

Net Impact on the Logistics Industry Amid Current Geopolitical Tensions

2026-01-18 06:54:59

Net Impact on the Logistics Industry Amid Current Geopolitical Tensions

2026-01-18 06:54:59

-

ITR (Income Tax Return) forms on the basis of Income Category

2025-05-13 20:05:27

ITR (Income Tax Return) forms on the basis of Income Category

2025-05-13 20:05:27

-

RBI’s Latest Guidelines on Bank Accounts & Deposits (2025 Update)

2025-06-08 11:48:55

RBI’s Latest Guidelines on Bank Accounts & Deposits (2025 Update)

2025-06-08 11:48:55