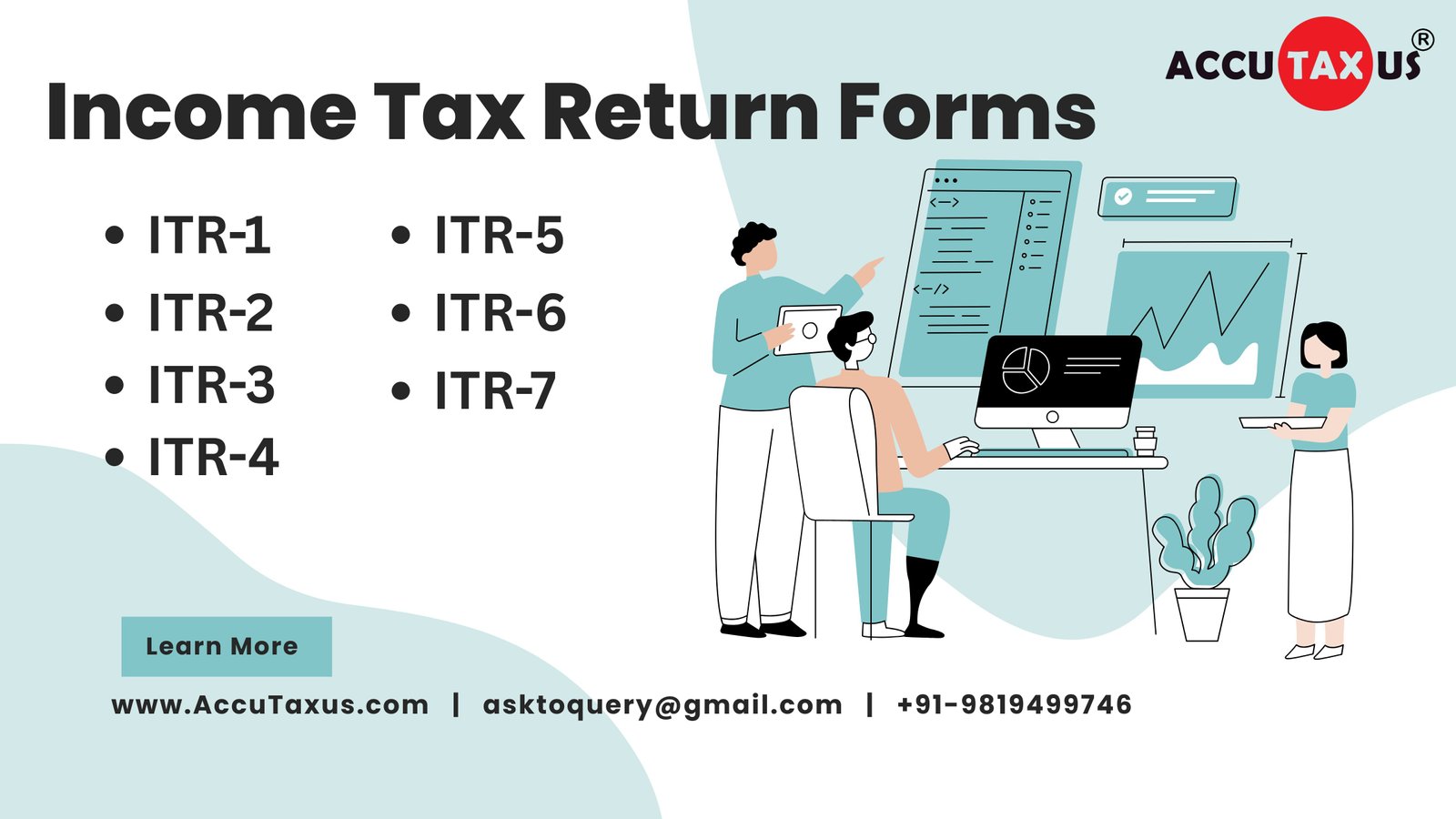

ITR (Income Tax Return) forms on the basis of Income Category

ITR (Income Tax Return) forms are chosen based on the taxpayer's type of income, total income, and other applicable criteria. Below is a bullet-point categorization of each ITR form by income details:

A- ITR-1 (Sahaj)-

a. For resident individuals (not HUF, not company, not director in a company, no investment in unlisted equity shares)

- Total income up to ₹50 lakh

- Income sources allowed:

- Salary or pension

- One house property (not more)

- Other sources (interest, etc.; excluding lottery or horse race winnings)

- Agricultural income up to ₹5,000

- Cannot be used if:

- Income exceeds ₹50 lakh

- Income from more than one house property

- Capital gains income (excluding long-term capital gains up to ₹1.25 lakh from listed equities)

- Income from business/profession

- Foreign income/assets

- Director in a company or investment in unlisted shares

B- ITR-2

- For individuals and HUFs (of which not having income from business/profession)

- No Total Income limit (can be more than ₹50 lakh)

- Income sources allowed:

- Salary or pension

- More than one house property

- Capital gains (short or long term)

- Other sources (including lottery, horse race winnings)

- Foreign assets/income

- Agricultural income exceeding ₹5,000

d. Cannot be used if:

- Income from business or profession (proprietorship)

C- ITR-3

- For individuals and HUFs with income from business or profession (proprietorship)

- No income limit

- Income sources allowed:

- Salary or pension

- House property

- Capital gains

- Business or professional income (including as a partner in a firm)

- Other sources

- Foreign assets/income

- For partners in a firm, directors in a company, or those with investments in unlisted equity shares

D- ITR-4 (Sugam)

- For resident individuals, HUFs, and firms (other than LLPs) opting for presumptive taxation (Sections 44AD, 44ADA, 44AE)

- Total income up to ₹50 lakh

- Income sources allowed:

- Business or profession (presumptive income)

- Salary or pension

- One house property

- Other sources (excluding lottery/horse race winnings)

- Agricultural income up to ₹5,000

- LTCG up to ₹1.25 lakh from listed equities (from AY 2025-26)

- Cannot be used if:

- Income exceeds ₹50 lakh

- Director in a company or investment in unlisted equity shares

- More than one house property

- Foreign income/assets

E- ITR-5

- For firms, LLPs, AOPs, BOIs, cooperative societies, local authorities, artificial juridical persons, estates of deceased/insolvent, business trusts, investment funds (not for individuals, HUFs, or those filing ITR-7)

- No income limit

- Income from any head of income tax(business or profession income, capital gains, house property, other sources)

F- ITR-6

- For companies (except those claiming exemption under Section 11 of the Income Tax Act, 1961 - income from property held for charitable/religious purposes)

- No income limit

- Income from any source

G- ITR-7

- For persons including companies required to file returns under sections 139(4A), 139(4B), 139(4C), 139(4D) (mainly trusts, political parties, charitable/religious institutions, specified entities)

- No income limit

- Income from property held under trust, charitable/religious purposes, political parties, research associations, etc.

Disclaimer: - The content on this blog is intended for general informational purposes only and should not be considered professional advice. While we strive to ensure the accuracy and timeliness of the content, tax laws and regulations are subject to frequent changes and interpretations. Readers are advised to consult with a qualified tax professional or financial advisor before making any decisions or taking any actions based on the information provided on this blog. The authors and publishers of this blog are not liable for any loss or damage resulting from reliance on the information provided.

Trending Posts

-

Annual Survey of Incorporated Services Sector Enterprises (ASISSE)

2026-07-02 04:06:05

Annual Survey of Incorporated Services Sector Enterprises (ASISSE)

2026-07-02 04:06:05

-

ITR Filing Guide for Govt Employees in Delhi NCR

2026-06-23 12:19:45

ITR Filing Guide for Govt Employees in Delhi NCR

2026-06-23 12:19:45

-

Net Impact on the Logistics Industry Amid Current Geopolitical Tensions

2026-01-18 06:54:59

Net Impact on the Logistics Industry Amid Current Geopolitical Tensions

2026-01-18 06:54:59

-

ITR (Income Tax Return) forms on the basis of Income Category

2025-05-13 20:05:27

-

RBI’s Latest Guidelines on Bank Accounts & Deposits (2025 Update)

2025-06-08 11:48:55

RBI’s Latest Guidelines on Bank Accounts & Deposits (2025 Update)

2025-06-08 11:48:55